Most credit card issuers calculate interest charges using a method called the 'average daily balance'. In order to find the sum, you multiply the mean outstanding balance on your bill at the end of each day by the Daily Periodic Rate(DPR) and the number of days in your billing cycle. The entire process involves quite a bit of jargon and basic arithmetic. This guide is meant to help you understand each step of the calculation, as well as explaining key terms to know.

Calculating Credit Card Interest (APR) Step by Step

Calculating credit card interest is an involved process. It requires a pen, paper and calculator— or, for more technical users, Excel or other computer tools can work as well. There are four steps to the calculation, which we have discussed below. Of the four steps, finding your average daily balance will be the most challenging. It requires you to know exactly what your balance was at the end of each day during the last billing cycle. If you're not interested in the details at all, we recommend using our interest calculator instead.

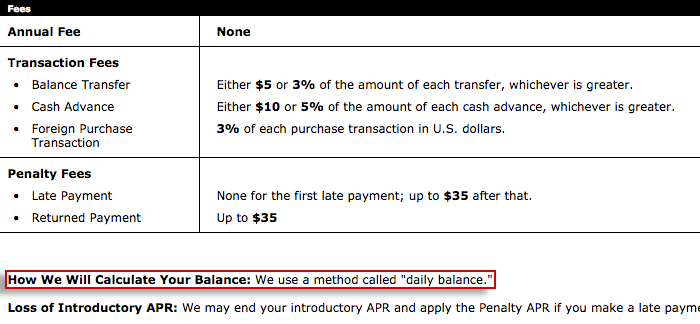

Step 1. Figure out how often your credit card interest is compounded. This means how often the interest is added onto your principal, or original, balance. Most credit card issuers today compound interest on a daily basis. You can find out what your particular bank uses by looking it up in the pricing information of your card, sometimes called the Schumer Box. Look for the line "How We Will Calculate Your Balance." All consumer credit cards are required to include this information there. If the document says it uses a method called "daily balance", your interest is compounded daily.

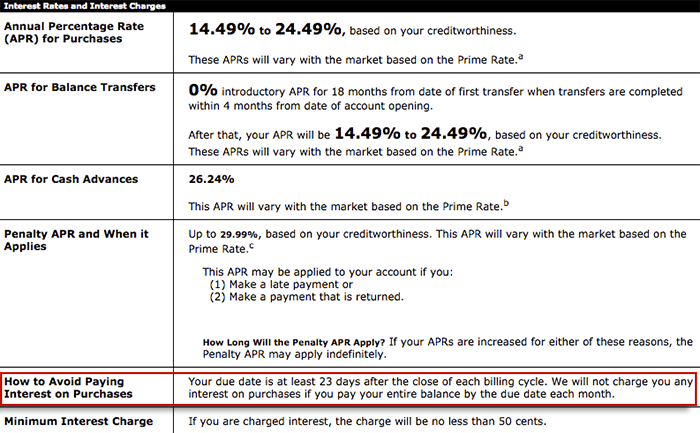

Step 2. Divide your card's annual percentage rate (APR) to get the periodic rate. If your issuer uses a daily balance, divide the APR by 365. If the APR is compounded monthly, divide it by 12. For example, an APR of 14.99% compounded daily would have a periodic rate of (14.99% / 365) = 0.0004 = 0.04%. Remember that when dividing percentages with a calculator you need to convert them to a decimal—that means dividing them first by 100. Therefore, when written out fully, the previous calculation is (14.99 / 100) / 365.

Step 3. Find your average daily balance. This step requires you to know exactly what your end-of-day balance was each day within a billing cycle. For example, let's say that for the first three days you had a $300 balance on your card, then it went up to $500 for the next 15 days, and finally up to $1,000 for the last seven days. Your average daily balance would be $616. This is calculated using the following formula:

(Day 1 Balance + Day 2 Balance + Day 3 Balance…) / total number of days in the billing cycle

Step 4. The final step is to put everything together. Multiply the periodic rate (Step 2) by the average daily balance (Step 3) and the number of days in your billing cycle. The result is the interest accrued by a credit card for a given period.

Note: Most credit cards have a minimum interest charge. The amount varies by bank, but is generally between $1 and $2. Therefore, if you follow the calculations outlined here and get an interest charge of $0.50, you're likely to pay more.

Example calculation

Card A charges a 14.99% APR. For a given month, the card's balance was as follows:

| Day(s) | Activity | Balance |

|---|---|---|

| 1-4 | None | $0 |

| 5-10 | $200 purchase | $200 |

| 11-13 | $50 purchase | $250 |

| 14-18 | $500 purchase | $750 |

| 19 | $400 payment | $350 |

| 20 -25 | $200 purchase | $550 |

Given the above debt breakdown, the average daily balance for the card is:

( (5$0) + (6$200) + (3$250) + (5$750) + (1$350) + (6$550) ) / 25 = $374

To calculate the interest for the 25-day period, we multiply the average daily balance by the daily periodic rate and the number of days in the billing cycle. The DPR in this case is 14.99% / 365 = 0.038%. The average daily balance is $374, and the number of days in the billing cycle is 25. Putting all that together we get: $374 * 25 * 0.038% = $3.59.

Accounting for Grace Periods

Consumer credit cards are required, by law, to give cardholders a set period of time to pay off their balance. Over the course of this so-called grace period, any new purchases added to the balance do not accrue interest. Therefore, if you manage to pay off your credit card bill within this grace period, you will not be charged any interest.

According to the CARD Act of 2009, you have 21 days to pay off your balance before interest starts to accrue. This time applies from the moment your bill is delivered to you—whether by mail or electronically. If your due date falls on a weekend or federal holiday, you have until the following business day at 5 p.m. to submit your payment.

Credit Card APR Calculator

We've built a credit card interest calculator to help facilitate your calculations. Add as many credit card balances as you'd like below, along with their respective interest rates and the type of monthly payments you make. The calculator will show what your total interest payments will be, by the time you completely finish paying off your debt.