Cards that offer a 0% annual percentage rate (APR) during an introductory period can help you save money by allowing you to skip interest charges on your purchases for a year or more. That’s an alluring feature. But here’s what else you need to know about these cards to make the most, and avoid the worst, about them.

They may not blare their low APR. There are cards, known as balance transfer cards, that also offer a 0% APR, and for a limited period (on a balance you transfer from another card--hence the name). But where balance transfer cards are all about their interest rate, and have few other features, regular cards with 0% APR may be fine choices in other ways, such as offering rich rewards.

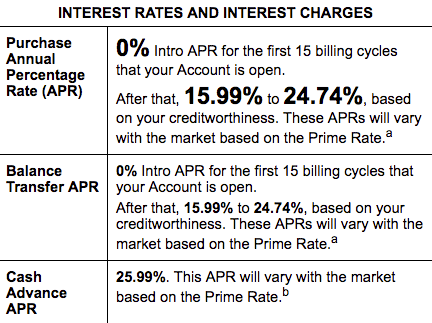

By contrast, these cards are the soft-spoken guests in the generally loud party that is the credit-card marketplace. In fact, you may not even know they offer a low interest rate unless you go looking. To know for sure whether a card is running this introductory perk, look for what’s known offer's Schumer Box—accessible by clicking 'Pricing & Terms' or something similar on a credit card's bank landing page. The first part of a Schumer Box details a card's interest rates and interest charges. The APR is broken down by the type of transaction—a purchase, a balance transfer or a cash advance.

Pay late? Lose the rate, potentially. This is another reason it’s worth delving into the fine print of your credit card agreement, this time to read its terms and conditions. That enticing 0% APR offer can be terminated if you violate any of these--which can happen if, for example, if you fail to make a minimum payment by its due date.

Should that happen, however, your APR on purchases you’ve already made will not jump up to the “regular rate.” Rather, that higher rate will apply to any purchases made after your misstep.

Only purchases get the 0% rate. Unless otherwise noted in the terms and conditions, you will still be charged interest on transactions other than new purchases. Notably, don’t take out a cash advance on a 0% card and expect to get what would amount to a free loan; the money you receive will almost certainly be subject to the same (stiff) APR as a cash advance on a card without a promotional APR.

The regular APR applies after the promo period ends. And not just to new purchases after that date, but to any balance you carry on the card past the end of the promotion. For example, if you buy a new TV set 9 months into a 12-month 0% period, you won't pay any interest for the first 3 months in which you carry its cost on your balance. From the fourth month, though, interest will begin to accumulate at the regular rate on the unpaid balance.

Cards with 0% APR are different—and mostly better—than deferred-interest cards. These two card types are similar, in that they allow you to skip paying interest for a certain period. The card flavors become very different, however, when the promotional period ends.

With a 0% APR card, if you fail to pay off a purchase that was made during the 0% period, you won't be charged interest retroactively. By contrast, should you still be carrying a balance on a deferred interest credit card at the time the no-interest period runs out, finance charges will be applied retroactively, back to the beginning of the promotion period.

Needless to say, make sure you’re absolutely clear on whether the card you get is a 0% APR card or one with a deferred interest promotion. One clue: deferred interest offers are most commonly extended with store credit cards. The Consumer Financial Protection Bureau (CFPB) has recently put out an advisory asking retailers to make this distinction clearer.

The irony, according to one study, is that ignorance appears to be a leading reason that many consumers pay those retroactive charges. The study, by the CFPB, found that many pay off the balances shortly after the promotional period ends, and the deferred interest charges hit their account. According to the agency, the finance charges catch many cardholders by surprise.

Credit Cards http://res.cloudinary.com/value-penguin/image/upload/v1507144281/GettyImages-511933188_hvjlg6.jpg